The Role of the VCM in Scaling CDR: Trends and Opportunities

As of today, the Voluntary Carbon Market (VCM) is a vital driver of demand for carbon dioxide removal (CDR). The VCM, in which private actors from individuals to organisations can purchase or trade carbon credits, both helps companies meet voluntary targets and provide financing for various removal pathways. While compliance markets remain crucial for long-term scaling of carbon removal, the VCM is currently the main driver of CDR demand and has already demonstrated its potential to accelerate progress. A key question is whether VCM's current trajectory and mechanisms are sufficient to scale CDR, or whether opportunities have been missed to scale CDR and support companies advancing their net-zero goals.

You're listening to:

Kathryn has a MSc in Climate Change from the University of Copenhagen specialising in climate policy and sustainability. She has experience in science communications and impact reporting, placing her expertise in between climate change and communications. A self-proclaimed geopolitics nerd, Kathryn uses this knowledge to track and brief our community on news and updates in and around the carbon removal space.

Simon has over ten years experience advising leading corporates and public organisations on climate and sustainability. With combined expertise on land-based projects and the carbon removal industry, he leads the side of Klimate focused on delivering impact. Simon brings this deep knowledge to an advisory role on critical topics including future of the market, company strategy, and regulatory affairs.

What is the Current State of the VCM?

The VCM has grown significantly over the past decade, with buyers increasingly shifting from avoidance to removal credits. CDR purchases are trending up—Q2 2025 saw more tonnes contracted (15.48 million) than all prior quarters combined (13.6 million). Companies setting voluntary net zero targets, which require some CDR to achieve targets, nearly tripled (from 417 to 1,245) in the last year, demonstrating sustained ambition despite talk of a "net-zero recession".

The IPCC estimates 6 to 16 gigatonnes of removals are needed annually by mid-century; the market today delivers only a fraction of that. Scaling to this level would potentially create a $7-35 billion industry by 2030, a 3-15x multiple in the next 5 years, and a $1.2 trillion industry by 2050.

Despite significant growth, the reality drawn from the recent body of research is:

- Most companies have not set net-zero targets (although many have)

- There are growing concerns that companies with net zero targets are not on track to meet both near- and long-term targets

- Delivery of scope three targets is particularly challenging.

Barriers remain to widespread company buy-in. High prices, limited expertise, and a lack of standardised methodologies for assessing credit quality hinder widespread adoption of high-quality removal credits.

Buyer motivations and purchasing trends

Corporate participation in VCM is driven by various factors, primarily 1) making progress towards internal or externally committed climate goals or 2) demonstrating action across broader social and nature goals, linked to stakeholder pressure and brand value. These factors shape credit selection, pricing, and prioritisation of methods, but can also constrain how and when companies use carbon credits.

Most voluntary frameworks confine the use case of carbon credits to two areas: compensating for residual emissions (10%) with permanent removals, or beyond the value chain (BVCM) in the form of contributions that occur outside emissions accounting books. Neutralising residual emissions is likely to yield only 0.1-1.3 GtCO2e per year, yet it is the only case mandated by standards. BVCM could unlock millions in climate finance, but lacks the leverage to be a priority for many companies. While this doesn't reflect the entire picture of the VCM, without clear and significant incentives, current buyer behaviour is likely to be insufficient to scale CDR to be ready for future net zero.

Today’s corporate frameworks for net zero require two things: deep emission cuts (60-90%) and compensating residual emissions with CDR. However, no framework requires that companies scale the CDR sector in the near-term to meet 2050 needs, though SBTi is considering near-term scope 1 removal targets and has proposed a 'gold star' program for BVCM participants.

While frameworks recognise CDR as essential to net-zero, none incentivise building the sector now. This gap limits corporate climate finance and puts all target-setters at risk of missing their stated goal: limiting warming to 1.5-2°C.

Strategic opportunity: How the VCM can play a larger role in scaling CDR

The VCM is already playing a critical role in creating early demand for CDR. But, without near-term development of the market, net-zero progress is stalled. This is true for a broad spectrum of decarbonisation technologies and infrastructure beyond CDR. As mitigation outcomes stall, corporate climate leaders–and the standards that guide their actions–must incentivise scaling CDR in the near-term or risk missing net zero targets on a global and individual scale.

Further strategic buying behaviours can drive economies of scale and make CDR more affordable. This type of action not only scales CDR but actually helps companies meet interim climate targets, ensures companies stay on track while working to reduce their own emissions, and decarbonises in a cost-effective way in the long-run.

We’ll dive into these strategic CDR use-cases below, all of which have potential to create meaningful net-zero progress in the coming years 5, 10, or 15 years before residual emission compensation at 2050.

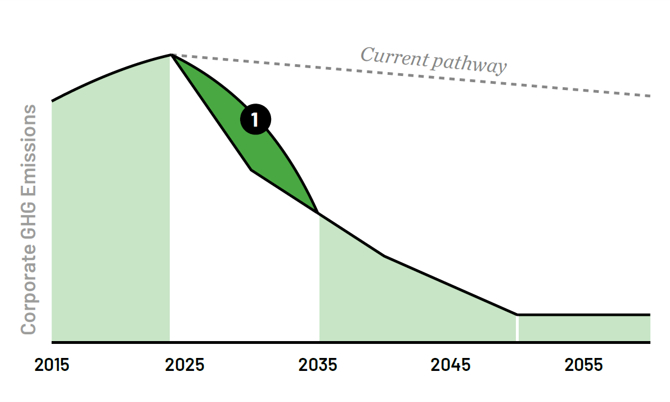

1. Closing the gap

Rather than and end-stage activity, CDR offers unique opportunities for companies to close the emissions gap between their internal reduction efforts and the necessary emissions removals. Many buyers have yet to fully leverage credits to fill near-term shortfalls in their decarbonisation path. Instead of considering CDR as a ‘maintenance’ activity at net zero, companies can create real decarbonisation progress, presenting strategic opportunity for participation in the VCM.

Using CDR to catch-up to commitments or statutory net zero targets would unlock massive financial potential for the market, and generate up to 5.9 GtCO2e of removals per year. More than unlocking finance, this effort would provide crucial, timely, climate mitigation to account for how internal decarbonisation has fallen short, noted in the significant gap between the dotted line and black line at the bottom of block 1.

2. Set & hit interim removal targets

Setting interim reduction and removal targets is a pragmatic approach to getting back on track to net-zero commitments. As noted above, an overly cautious approach to the sequence of reductions and then removals can result in stagnant years where no action happens at all. Setting, achieving, and clearly communicating interim targets every 5-10 years highlights ambition and accelerates global decarbonisation.

For example, let’s look at Company A’s journey to a 2050 net-zero target. Beginning in 2025, they measure a baseline of 100,000 tonnes CO2e annual emissions. A 2030 interim target could reduce emissions to 70,000 tonnes (a 30% reduction) and remove 5,000 tonnes through CDR credits. By 2035, they reduce emissions by 50% and remove 10,000 tonnes. This continues until 2050, when their reduction target equals their removal target—allowing them to neutralise remaining emissions with permanent removals. Setting these 5–10 year checkpoints keeps the company accountable, demonstrates continuous progress, and scales CDR purchasing gradually, giving the company experience with budgeting for carbon and effectively pricing their emissions.

3. Addressing ongoing emissions

A significant opportunity lies in addressing unabated emissions from sectors that continue to produce high carbon outputs despite best efforts at decarbonisation. For example, industries such as professional services, technology, and manufacturing are seeing large volumes of emissions in their Scope 3 categories. Taking responsibility for these is currently termed BVCM, or climate contribution, occurring outside emissions accounting.

Companies can address ongoing emissions by investing in contribution or removal credits that align with the yearly emission outputs–either with a 1 to 1 ratio, or a so-called money-for-tonne approach that covers a significant amount of a given company’s total tonnes while also directing finance into most critical areas. If companies quickly get back on track with their intended reductions, this lowers the cost of taking responsibility.

Depending on how quickly companies get back on track with their reduction targets, using credits to address ongoing emissions could unlock 0.27 to 3.2 GtCO2e of additional mitigation. But if corporate emissions reductions continue to lag, this figure could be much more. By deploying removal credits strategically in these sectors, companies can smooth the transition to net-zero while maintaining progress on their climate commitments.

4. Decarbonise within the value chain

Insetting is regarded as interventions within the value chain that result in a removal or permanent reduction. Methodologies and accounting for insetting programs are in development and vary across sector. However, this path offers an obvious win-win for decarbonisation and removal sector financing. Value chain removals could take the form of a grocery story investing in regenerative agriculture credits at one of their produce farms, or a construction company investing in and using mineralised concrete in a new build. By investing in credits or technologies that remove or permanently reduce the emissions of their own value chain, they can reduce their operational emissions, getting one step closer to net zero.

Tools, guardrails, and regulations

Beyond specific purchasing strategies, new procurement pathways are necessary to scale the VCM and make credits more accessible. Some examples include pooling smaller buyer demand, which can generate the volume needed to bring costs down, and bundling portfolios of credits to mitigate costs across different types of removals. Blended finance and other hybrid public-private mechanisms can reduce risks for emerging removal technologies. These tools improve affordability, enable portfolio diversification, and broaden market impact.

Linking voluntary credits to compliance systems, such as regulatory carve-outs for specific credit types, could make the market more liquid. Dual incentives for compliance and voluntary targets would amplify the VCM's role in global emissions reductions. Through a strengthened regulatory environment, standardised national approaches, and improved infrastructure, we build confidence in the market and remove barriers to exponential growth.

Ensuring a stronger role for the VCM in the future

The Voluntary Carbon Market is uniquely positioned to drive the scaling of CDR in the coming years. The voluntary market can catalyse removal scale not only by providing financial support, but also by deploying more sophisticated procurement tools, price signals, and buyer behaviours that strengthen market dynamics and reduce risk. If we wait for mandatory frameworks alone (e.g., compliance markets), we risk both missing key scaling opportunities for CDR and climate mitigation outcomes. This creates an interesting relationship: the VCM is important to help decarbonising technologies scale, but also these technologies in turn help VCM actors achieve cost-effective net zero.

Further reading:

- The Nature Conservancy, Bending the Curve.

- IETA, VCM Guidelines 2.0.

Kathryn has a MSc in Climate Change from the University of Copenhagen specialising in climate policy and sustainability. She has experience in science communications and impact reporting, placing her expertise in between climate change and communications. A self-proclaimed geopolitics nerd, Kathryn uses this knowledge to track and brief our community on news and updates in and around the carbon removal space.

Simon has over ten years experience advising leading corporates and public organisations on climate and sustainability. With combined expertise on land-based projects and the carbon removal industry, he leads the side of Klimate focused on delivering impact. Simon brings this deep knowledge to an advisory role on critical topics including future of the market, company strategy, and regulatory affairs.

Discover the news shaping the future of carbon removal.

BVCM & SBTi: an essential strategy to address ongoing emissions

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Net zero strategy – what is it, and what does it include?

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Understanding carbon offsets: The difference between avoidance and removal credits

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Sign up for Klimate Insights

Every second month we'll send you an update on all things Klimate, carbon removal, and the most important emerging news and policy.

Talk to a carbon removal strategist

Finding the right way to remove your CO₂ emissions can seem overwhelming. Our team is here to help. Book a meeting to walk through how our solution might fit your needs.